Published:

Mar 3, 2016

Updated:

Analysis of revenue recognition for nonrefundable upfront fees under ASC 606, including when the fees relate to specific performance obligations or material rights.

In many circumstances, companies require customers to pay nonrefundable upfront fees. Examples include membership fees for a health club or an activation fee for cable, internet, or telephone services. Should revenue be recognized immediately or deferred over time? If the revenue should be deferred, over what time period should the revenue be deferred?

The revenue standard addresses this issue in Accounting Standards Codification (ASC) 606-10-55-51:

To identify performance obligations in such contracts, an entity should assess whether the fee relates to the transfer of a promised good or service. In many cases, even though a nonrefundable upfront fee relates to an activity that the entity is required to undertake at or near contract inception to fulfill the contract, that activity does not result in the transfer of a promised good or service to the customer. Instead, the upfront fee is an advance payment for future goods or services and, therefore, would be recognized as revenue when those future goods or services are provided.

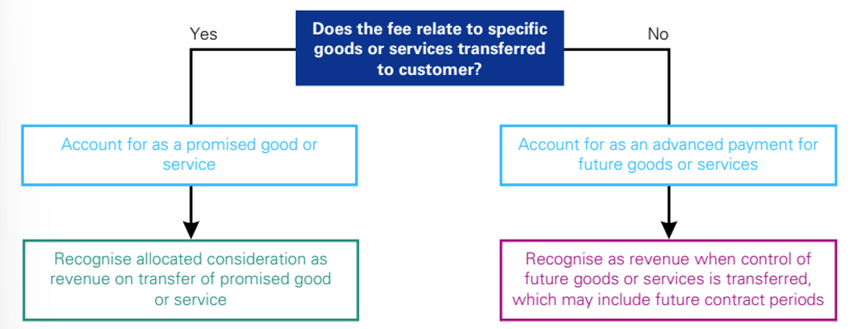

The consideration received in connection with nonrefundable upfront fees should be added to the other consideration received in the contract. The total amount of consideration the entity expects to receive should then be allocated to the distinct performance obligations. In some cases, there may be a distinct performance obligation in connection with the upfront fee. If the fee is related to a distinct performance obligation, the revenue will be allocated to that performance obligation based on its relative standalone selling price. That amount may or may not be the same as the upfront fee. This can result because the timing of payments does not always correlate to the timing of goods or services delivered. This flow chart from KPMG illustrates clearly the thought process that should take place. Notice that if the fee does relate to specific goods or services transferred to a customer (a performance obligation), the amount recognized is the consideration allocated to the performance obligation rather than the amount of the fee.

One issue relating to nonrefundable upfront fees arises when there is a contract renewal option that provides the customer with a material right. A material right is created when customers have an option to purchase additional goods or services for a material discount. For example, a material right is created when a health club charges a $100 membership fee upfront, in addition to $30 ongoing monthly payments for 1 year, but the contract allows for a renewal of the contract for additional years without another membership fee. The upfront fee does not relate to activities that transfer a good or service to the customer and does not represent a distinct performance obligation. The revenue associated with the fee would be allocated to the performance obligations within the contract, the gym service in this case, which is satisfied over the 12 months of the contract. If there is a renewal option that allows a customer to renew the one year contract without paying the additional fee, a material right may exist.

When evaluating if a material right exists, both quantitative and qualitative factors should be considered, as well as past and future transactions with the customer. If it is determined that the renewal option conveys a material right to the customer, the customer effectively pays in advance for additional goods or services, and the material right should be accounted for as a separate performance obligation. The entity should allocate revenue based on the relative standalone selling price of the option. Often, the standalone selling price of that option is not directly observable and must be estimated. See Standalone Selling Prices for additional discussion on the estimation of standalone selling prices. The associated revenue should then be recognized when that right is exercised or expires.

Although the standalone selling price of these options is often unobservable, a practical alternative to estimating the standalone selling price of the option can be found in ASC 606-10-55-45:

If a customer has a material right to acquire future goods or services and those goods or services are similar to the original goods or services in the contract and are provided in accordance with the terms of the original contract, then an entity may, as a practical alternative to estimating the standalone selling price of the option, allocate the transaction price to the optional goods or services by reference to the goods or services expected to be provided and the corresponding expected consideration. Typically, those types of options are for contract renewals.

This option is only available if the optional goods or services are similar to the goods or services being provided under the original contract. Using this approach, a company allocates the transaction price to the optional goods or services by spreading out the total amount of expected consideration over the entire period in which the entity expects to deliver those goods or services. For the example given above, the practical alternative would be available because the optional services, (the health clubs facilities and benefits), are the same as the services under the original contract. If the health club expects that the customer will renew the membership for one additional year, the company would recognize $34.17 each month for the 24 month period ((30*24 months + 100)/24 = 34.17).

The Transition Resource Group (TRG) met and discussed nonrefundable upfront fees as part of its discussion of customer options for additional goods and services, due to the assessment required under ASC 606 of whether or not a material right for future goods and services exists in the contract. See the “Diversity in Thought” section of Customer Options for Additional Good or Service for a discussion on the TRG’s deliberations on issues surrounding customer options and material rights.

The consideration received for a nonrefundable upfront fee should be added to the total consideration and allocated to the distinct performance obligations in the contract. Companies should analyze whether the nonrefundable fee creates a material right, which would be a distinct performance obligation to which consideration needs to be allocated. There may be changes in the way companies account for nonrefundable upfront fees based on whether or not the fee relates to a distinct performance obligation and whether or not the fee creates a material right.