Published Date:

Apr 7, 2016

Updated Date:

The prospective treatment method vs. the cumulative catch-up adjustment method of applying contract modification treatment under ASC 606.

Contract Modifications Part I introduced contract modifications and described the steps to determine whether a contract modification should be considered a separate contract. First, an entity determines whether a change to a contract qualifies as a contract modification. Second, the entity determines whether the change meets the requirements for treatment as a separate contract. A contract is considered separate when the change is comprised of the addition of distinct goods or services at a price comparable to their standalone selling prices. This article addresses proper accounting treatment for modifications that are not treated as separate contracts.

If the contract modification is not considered a separate contract, the modification is combined with the original contract. There are two methods to account for these contract modifications. An entity should choose the method that most appropriately aligns with the facts and patterns of the modified contract. The accounting model for contract modifications depends on the nature of all remaining goods and services at the time of the modification (not just those added by the modification).

If the remaining goods and services are distinct from those in the original contract, but the modification does not meet the other separate contract criteria (i.e., the additional goods are not sold at a price comparable to their standalone values), the entity treats the original contract as terminated and accounts for both the original contract and the modifications together as a newly created contract (Accounting Standards Codification (ASC) 606-10-25-13). Revenue already recognized on the original contract is not adjusted. All remaining transactions are accounted for on a prospective basis: unrecognized consideration is allocated to the remaining performance obligations.

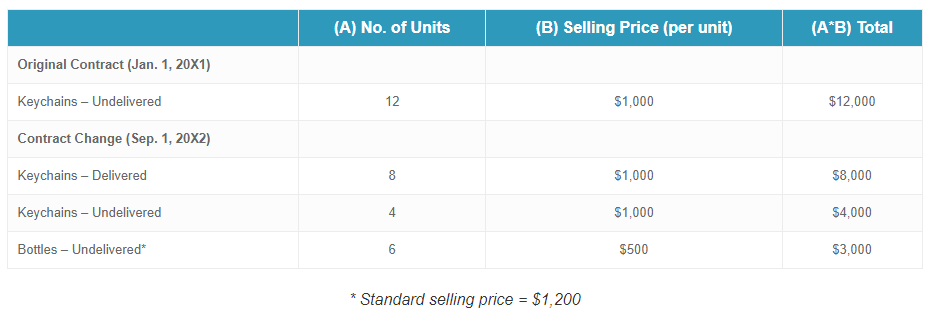

Example A: Prospective Treatment with an Equipment Delivery Contract

On January 1, 20X1, Equipment Company entered into a contract with Knickknack Maker to sell twelve units of manufacturing equipment used for producing keychains for $1,000 each (for a total contract price of $12,000).

The agreement outlines that Equipment Company will ship one unit of equipment every month for one year starting on January 1, 20X1. Revenue of $1,000 per unit is recognized on delivery. On September 1, 20X1, after delivery of the first eight units, Equipment Company agrees to a contract modification to deliver six units of equipment used to assemble water bottles. These items are distinct from the keychain units and are normally sold at $1,200 per unit. However, Equipment Company will sell these units to Knickknack at $500 each—this price is not comparable to the standalone selling price. Equipment Company will continue to recognize revenue from each unit separately on delivery. Equipment Company concludes that the delivered keychain equipment units are distinct from those still undelivered.

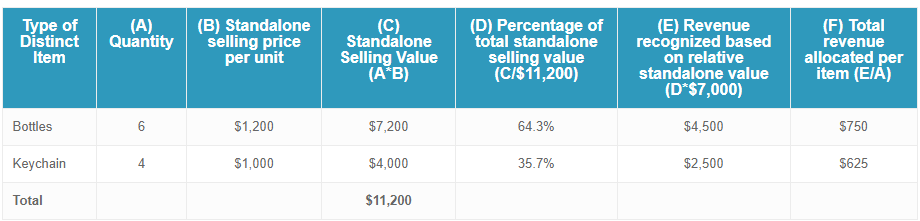

This contract modification should not be treated as a separate contract. Although there are additional, distinct goods being promised by Equipment Company, the price of those additional goods are not comparable to their standalone selling price. The original contract is considered terminated, but the $8,000 of revenue recognized up to this point on the already delivered units will not be adjusted. Instead, the performance obligations from the original contract and the obligations from the modification combine to create a new contract (with a total value of $7,000). Under the new contract, revenue is allocated to each item to be delivered based on its relative standalone selling price. As such, Equipment Company will recognize $750 for each bottle-maker, and $625 for each piece of keychain equipment. (For more information, see Standalone Selling Prices.)

If the remaining goods and services are not distinct, the entity combines the increase or decrease of goods or services with the original contract’s promised goods or services to create a single performance obligation that is partially satisfied at the date of the modification. The entity adjusts revenue previously recognized to reflect the changes of the modification to the transaction price. This ensures that revenue recognized measures progress toward completion of the performance obligation (on a cumulative catch-up basis).

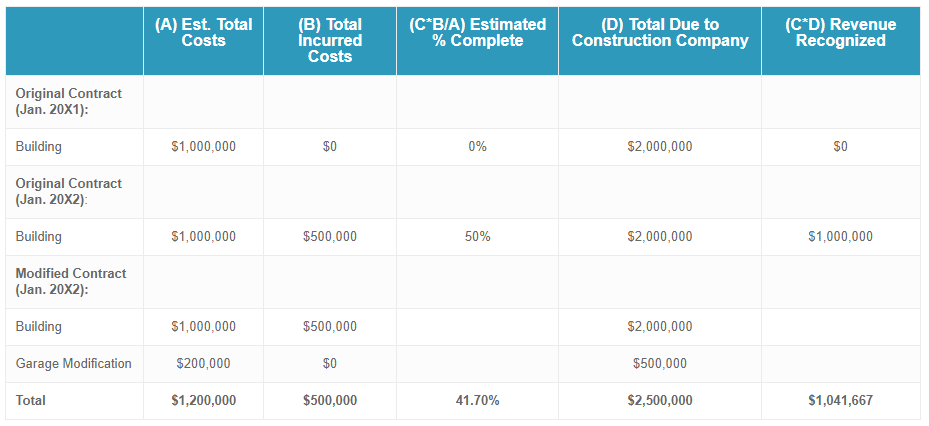

Example B: Cumulative Catch-Up Adjustment with a Construction Contract

Construction Company agrees to build an apartment complex for Grump Company on January 1, 20X1. The building will take 24 months to complete and will be built on land owned by Grump Company. Construction Company will receive consideration of $2 million. Construction Company accounts for the goods and services provided as a single performance obligation satisfied over time. It also determines that the most appropriate method to measure progress of completion is through the input measure of costs incurred.

Construction Company expects total costs to total $1 million. By January 1, 20X2, Construction Company had incurred $500,000 in costs related to the project and measured its progress toward completion at 50 percent. Construction Company has accordingly recognized revenue of $1 million to date. On this same date, Grump Company requested a change in the scope of the contract: to increase the size of the parking garage. The parties agreed that an additional $500,000 will be paid to Construction Company for this change. Construction Company estimated it would incur additional costs of $200,000 as a result of the changes. It is also estimated that the changes will require an additional 6 months to complete construction. An analysis concludes that the additions are not distinct from the goods and services promised in the original or now-modified contracts. Therefore, the additional goods and services are part of the same performance obligation from the original contract.

Guidance for contract modifications under ASC 605 varied between industries, but was most extensive for change orders and claims for construction- and production-type contracts (ASC 605-35). This shares some similarities with the guidance under ASC 606. As most other industries did not have as extensive authoritative 605 guidance, entities relied on guidance from accounting firms and followed their own, internally generated policies. Under ASC 606, entities will need to critically evaluate their longstanding practices and policies. This could lead to major changes in accounting policies (or few, if any, changes) depending on how closely aligned an entity’s accounting for contract modifications is to ASC 606.

It is unlikely that construction- and production-type industries will see major changes when accounting for changes to a contract. ASC 605-35 has similar requirements of additional, distinct promised goods and services at a comparable price in order for a change to be a separate contract. However, all entities will need to carefully examine modified contracts that were considered completed under ASC 605 because performance obligations associated with those modifications may be considered unsatisfied under ASC 606 (for more on this, see Contract Modifications – The Hindsight Expedient).

ASC 606 provides authoritative guidance to a subject that, in many industries, had none. Under ASC 605, many entities relied on firm guidance and other non-authoritative sources to develop accounting policies for contract modifications. The transition to 606 forces entities to review longstanding policies and practices to ensure they are in line with authoritative guidance.

If the goods or services remaining after a contract modification are distinct from those in the original contract, but are not provided at comparable standalone selling prices, the original contract is treated as terminated; the original contract’s remaining performance obligations and the modification are accounted for as one, single, partially-completed contract without any adjustments to revenue. If there are no distinct goods or services provided, the modification is combined with the original contract by adjusting revenue on a cumulative catch-up basis.

Companies are dealing with impracticalities of transition guidance pertaining to contract modifications. Some find it costly and overly difficult to retrospectively apply this guidance to all their contract modifications because they have numerous decades-long contracts with multiple modifications. The Financial Accounting Standards Board (FASB) has proposed a tentative practical expedient to help transition from ASC 605 to ASC 606. For more on the practical expedient, see Contract Modifications Part III– The Hindsight Expedient.